GIC’s annualised real return at highest since 2015; remains cautious amid uncertain environment

Singapore sovereign wealth fund GIC posted its highest returns since 2015 for the latest financial year, but said it remains cautious in an uncertain macro environment due to a protracted COVID-19 pandemic and stretched valuations.

SINGAPORE: Singapore sovereign wealth fund GIC posted its highest returns since 2015 for the latest financial year, but said it remains cautious in an uncertain macro environment due to a protracted COVID-19 pandemic and stretched valuations.

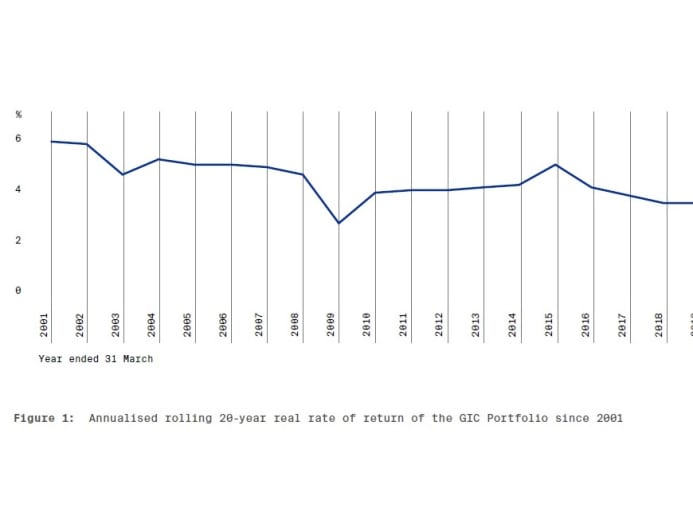

In its 2020/21 annual report released on Friday (Jul 23), GIC said its 20-year annualised real rate of return came in at 4.3 per cent for the year ended Mar 31. This is up from 2.7 per cent in the previous financial year and the highest since 2015 when real returns hit 4.9 per cent.

The 20-year metric – a primary indicator of GIC’s investment performance – is a “rolling” return where years are dropped and added as the computation window moves. For instance, the figure for FY2020/21 represented the average annual return of GIC’s portfolio between April 2001 and March 2021, with global inflation taken into account.

The spike in the real rate of return was partly due to the “poor year” in FY2000/01, caused by the dot-com crash, being dropped out of the 20-year window, said GIC’s chief executive officer Lim Chow Kiat during an online press briefing ahead of the report’s release.

The past year also saw a strong rebound in risk assets, such as global equities, on the back of policy actions and the development of COVID-19 vaccines, he added.

“Almost all the risk assets have done really well and even those assets which (had direct) negative impact from the pandemic actually held up reasonably well. So you had a lot of assets performing and that, I guess, contributed to the good performance of the portfolio,” Mr Lim told reporters.

Nominal bonds and cash, which are generally seen as safer investments, accounted for the biggest share of GIC’s portfolio at 39 per cent at the end of the last financial year, a drop from 44 per cent a year ago.

This corresponded with higher allocations to emerging market equities (17 per cent) and private equity (15 per cent), which increased by two percentage points each.

The allocation to real estate also went up slightly from 7 per cent to 8 per cent.

Inflation-linked bonds and developed market equities form the other asset classes in the portfolio - both of which remained unchanged in terms of compositions.

By geography, GIC holds slightly more than one-third (34 per cent) of its assets in United States as at the end of the last financial year. Asia (excluding Japan) forms 26 per cent, while Japan makes up 8 per cent.

The rest of the portfolio is distributed among markets such as the United Kingdom, Eurozone, Latin America, Middle East, Africa and the rest of Europe, as well as rest of the world.

This “diversified portfolio and cautious investment stance” has continued into FY2020/21 given elevated asset valuations and uncertainty from potential inflationary pressures, GIC said in its report.

GIC, which marks its 40-year anniversary this year, is one of three entities managing Singapore’s reserves. The other two are the Monetary Authority of Singapore and Temasek Holdings.

It is the Government’s fund manager. It does not own the assets it manages and does not invest in Singapore.

READ: Temasek’s net portfolio value rebounds to record high

Temasek released its latest annual report last week, which saw its portfolio value hit a record high of S$381 billion.

CAUTIOUS ON MACRO ENVIRONMENT

While GIC’s portfolio performance has remained resilient, the sovereign wealth fund warned of several uncertainties in the medium term, including the trajectory of the pandemic, elevated asset valuations, as well as fragile fundamentals in the global economy and less policy room.

This could weigh on returns as Mr Lim wrote in the report: “Given the uncertain macro environment and stretched valuations, we expect returns from a broad range of asset classes to be low for the next five to 10 years.”

Elaborating on these uncertainties, GIC’s group chief investment officer Jeffrey Jaensubhakij cited concerns about how vaccines are still not fully available in all parts of the world and the different COVID-19 variants “could continue to develop in a worrying way”.

While some recovery could occur in the near term, aided by factors such as fiscal stimulus and continued low interest rates, this will be “accompanied by some supply constraints where not everybody can come back to work”.

“As a result, there are shortages allowing for inflation to pick up. We've seen that in commodities. We’ve seen that in some of the wage rates in the US and so on,” said Dr Jaensubhakij.

“And those inflation concerns ultimately will bear on central banks’ decision-making and policymaking, and they may have to raise interest rates, which of course takes away some of the positive impact.”

Meanwhile, elevated equity and risk asset valuations will also be “a facet of the medium-term”, implying “probably low and rather volatile returns” going forward, he said.

“So we are macro-cautious for the medium term,” he told reporters.

POSITIVE “MICRO” OPPORTUNITIES

Still, GIC said it is “micro-positive” on a number of opportunities.

One of them is the accelerating technological transformation that is set to disrupt many industries, lower costs and increase productivity.

GIC remains a long-term investor in this field, Dr Jaensubhakij said. “We have several groups in different geographies looking at the opportunities there and we think that, in fact, there will be more to come.”

Sustainability is also a key priority for the Singapore sovereign wealth fund, which expects consumers and governments to “continue emphasising the importance of climate-friendly practices”.

“As a long-term investor, we seek to invest into this trend whilst protecting our portfolio assets from being negatively affected,” GIC’s report said.

“Integrate sustainability into our portfolio and investment processes holistically, taking into account the diversity of the industries and markets we operate in; and engage and support our investees and partners in their transition towards sustainability,” it added.

GIC launched the Sustainable Investment Fund in July last year as a “dedicated investment portfolio to accelerate sustainability integration across all asset classes”.

This is an “internal effort coordinated across both public and private markets to identify and invest in sustainability-related opportunities that generate good financial risk-returns over time”, its report said.

Asked how GIC plans to stay ahead of these opportunities given that these are also themes eyed by other investors, Dr Jaensubhakij said the Singapore sovereign wealth fund has three advantages.

First, GIC is a long-term investor.

“It means that when things have gotten too expensive, we’re not forced to chase after expensive low-return investments. Likewise, when there is more concern or fear, which is likely to be temporary, we can also step in and say ‘maybe the fear can continue for a year or two but in the long run, these investments should recover’,” he said.

“So we hope to take as much advantage as we can out of that long-term capability to find good investments.”

Second, it is banking on the “breadth and the depth” of its employees which work out of nine other offices outside of Singapore and look at opportunities across multiple asset classes. GIC is also opening a new office in Sydney next year.

READ: Singapore's GIC to open new office in Sydney in 2022

Third, GIC is invested with “some of the best investors and partners that are also looking for leads”, said Dr Jaensubhakij. “So, it's not just what we can do but also what our partners are doing and so on.”

“It is very competitive. I don’t want to make little of that but I think we are going to lean on whatever advantage we can muster around our partnerships, our local teams and our long-term capabilities to try to find those opportunities,” he added.

GIC also continues to see potential in Asia. Apart from positive growth prospects, other reasons include the region’s central bank policies being “quite conservative, responsible” and the presence of more attractive asset valuations.

“A lot of the recovery that has occurred took place also in countries where valuations were already high so the high has gotten even higher. The US, in particular, has benefited a lot,” Dr Jaensubhakij said.

“The relative valuations of US companies versus European versus Asian has continued to widen … So we’ve found that Asian companies have remained attractive on a relative basis.”