commentary Commentary

Commentary: Why Grab is in such a rush to get listed

CEO Anthony Tan is in a rush to build Grab into a super app and achieve profitability, and the company’s listings will help him do that without too much public scrutiny, say IMD Business School’s Howard Yu and Angelo Boutalikakis.

A man walks past a Grab office in Singapore. (File photo: Reuters/Edgar Su)

LAUSANNE: Grab battled Uber. It survived a merger fallout with Gojek. It coaxed tolerance out of regulators in a fragmented region of Southeast Asia.

Most recently, the Securities and Exchange Commission (SEC) has threatened to put a brake on the frantic SPAC (special purpose acquisition companies) activities. Despite all this, Grab managed to land a US$40 billion merger with the US-based Altimeter Capital.

“You need to be hyper paranoid and constantly thinking that the guy on your right is trying to murder you,” CEO Anthony Tan of Grab said in an interview with Financial Times in 2014.

READ: Commentary: Anthony Tan, the ‘unabashedly ambitious’ man behind Grab

His paranoia has been justified - Anthony is restless. His “workhorse” nature has been known since his days at Harvard Business School. He has been seen taking calls and reading case studies while running on a treadmill.

What he’s running against now is time. He needs Grab to become a super app before others. He needs to do so before Grab’s core business shows any signs of plateauing.

TOO MUCH MONEY IS CHASING TOO FEW GREAT IDEAS

The rise of SPACs is closely tied to one of the biggest wealth transfers of modern economic times. The purpose of a SPAC is to raise capital through an initial public offering (IPO).

Only later will a SPAC buy a start-up.

READ: Commentary: Grab’s blockbuster deal comes at questionable time for SPAC market

In this twisted arrangement, the start-up can effectively bypass all the compliance hurdles of a traditional IPO.

There’s no public scrutiny of financial disclosure and no formal filing of a detailed prospectus in the form of S-1. That’s why SPACs are referred to as blank cheque companies. They give whatever a start-up needs without asking too many questions.

For instance, through a regular IPO, Mr Tan would have faced lots of challenges in securing his 60.4 per cent voting rights that he has once the company is listed even though he only owns 2.2 per cent of ordinary shares.

The recent experiences of the founders of WeWork and Deliveroo show that investors can scupper such disproportionate control of power in an IPO.

During most of financial history, SPACs had been a minor play. After all, what respectable investors are going to put money in a shell company in the hope that it would one day successfully pick a high-flying unicorn? But the COVID-19 crisis changed all that.

Multi-trillion-dollar stimulus packages have flooded the market with liquidity never seen before. The record highs of Dow Jones and Nasdaq mean that the wealthy - family offices and hedge funds -have become obscenely wealthier.

READ: Commentary: Deliveroo’s IPO is a lesson to not underestimate investors

Meanwhile, the number of publicly listed companies has been dropping over the last three decades, dropping from 8,000 to just over 4,000 today. All that money needs to find new investment opportunities.

So, Altimeter Capital becomes the blank cheque company for Grab. And in this deal, Grab will receive a maximum of about US$4.5 billion in cash from the SPAC merger.

A BIG BUSINESS THAT MAKES NO MONEY

For Grab though, there may be other reasons why the SPAC route was preferred, to escape public scrutiny over financial disclosure compulsory under an IPO.

For venture capitalists or the financial market, no business model is more attractive than a platform - a marketplace that enables the exchange of goods or services and has purported “network effects”.

READ: Commentary: What’s behind Grab’s reported SPAC listing

This so-called network effect has been a common refrain among economists and academics to explain the spectacular growth of these businesses.

They argue the more people use a platform, the more inherently attractive it becomes, leading even more people to use it. And once a platform reaches a certain size, it becomes too dominant to unseat.

The problem is this argument ignores the profitability issue. In ride-sharing, it turns out that the mere presence of one additional competitor can lead to ruinous, undifferentiated competition.

Plus ride-sharing’s network effect is also limited within one location. For instance, if you are using Grab in Singapore, you don’t necessarily care about the service level in Manila.

This is unlike Facebook, which has a global network. It is also difficult for another company to give Airbnb, for example, a run for its money as that competitor needs to have a global reach and network that Airbnb has. For companies like Grab, competition can easily spring up locally.

Advertisers like P&G or Nike actually care a lot about the size of Facebook’s audience from London to Hong Kong and so companies like Grab who don’t have that global network lose out on large advertising money.

As a result of a more open playing field locally, ride-sharing can easily succumb to a price war. Discount coupons and driver incentives quickly eat into profit margins.

That’s how Grab, Gojek, Uber, and Lyft have lost money.

But Uber in Southeast Asia is no more. And so the bleeding on that front has stopped.

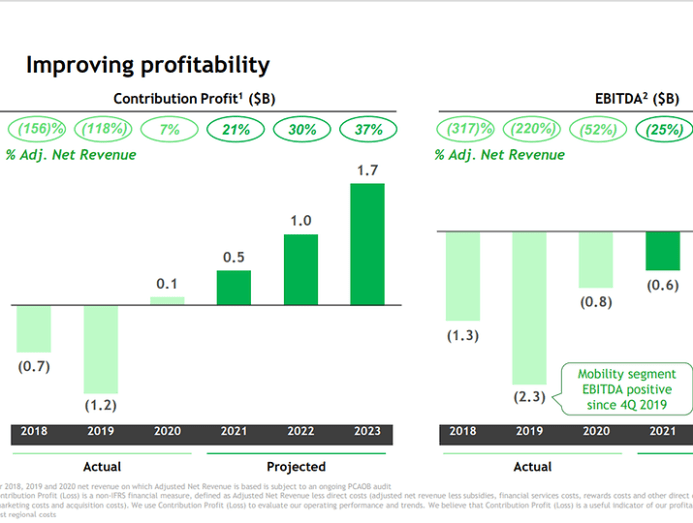

Yet here is exactly why Grab prefers the SPAC route. According to the details revealed in its investor presentation, Grab will have to shave off hundreds of millions of dollars each year, in order to reach profitability.

It only aims to get to positive EBITDA (earnings before interest, tax, depreciation and amortisation) in 2023.

READ: Commentary: What is the logic of AirAsia entering Singapore’s food delivery market?

READ: Commentary: The gig economy – a surprise boost from the pandemic and in Singapore, it’s not going anywhere

How will it do that? Grab’s ride-hailing business – which achieved positive EBITDA just last year - shows the way.

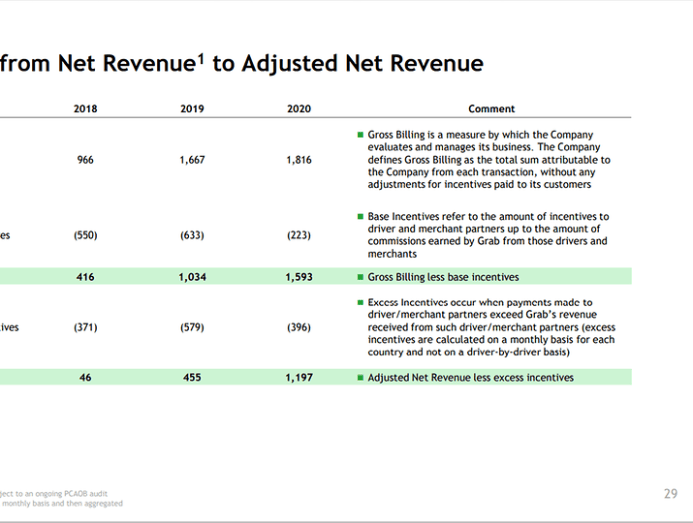

Already, to save costs in 2020, it may have cut off more than S$600 million worth of incentives for drivers and merchants – a figure larger than the increase it earned in billings that year.

No surprises then if Grab slashes incentives further to achieve the targeted profitability in the next few years. Such information, if disclosed through an IPO prospectus, may have seen a public backlash, which could have affected its listing returns or share pricing.

The question is, can Grab still maintain market share in the currently loss-making food delivery business if it cuts incentives? Why wouldn’t Foodpanda, Deliveroo and others swoop in to scoop up the clientele? Why wouldn’t people simply switch when Foodpanda has full-time deliverers on shifts and therefore may be potentially more reliable?

Regardless, these shaky profitability concerns are also why Mr Tan must move Grab into online food delivery, which since last year is now the biggest contributor to the company’s revenue.

This brings us to Grab’s second listing in Singapore.

FINTECH IS WHERE THE MONEY LIES

Today, Grab is expanding into a “super app.” It offers everything from food and parcel delivery to hotels and airline bookings and access to financial and health services. But being a super app can’t promise profitability; only being in the financial sector does.

It’s a sector full of slow-moving incumbents - and one stuck with obscenely high margins. And most attractive of all, it’s an industry teeming with paperwork and manual processes that should have been automated through technologies decades ago.

And Singapore, being the financial hub, will be Grab’s toehold for its financial service ambition. It has already acquired a banking license together with Singtel.

READ: Commentary: Why a bumper crop of Southeast Asian tech unicorns look set to IPO this year

That’s also why Mr Tan is also considering a second listing in Singapore. He doesn’t need additional money, but a second listing will buy him goodwill from the Singapore Government.

Grab has already acquired a banking license together with Singtel in Singapore, which as a financial hub, will be Grab’s toehold for its financial service ambition. However, Grab will need ongoing accommodation from regulators to navigate any resistance from traditional banks.

Since the company has sufficient cash reserves, it would only raise a small amount on the SGX, but this very symbolic listing would mark a big win for the Singapore Exchange.

The deal will put SGX in the international spotlight to rival its bigger counterpart of Hong Kong.

Because in Asia, you “had to work with individual government stakeholders, people of power and influence, in the highest echelons,” said Anthony.

It’s never too early to buy public goodwill.

Howard Yu is the author of LEAP: How to Thrive in a World Where Everything Can Be Copied (PublicAffairs; June 2018), LEGO professor of management and innovation at the IMD Business School in Switzerland, and director of IMD’s signature Advanced Management Program. Angelo Boutalikakis is a research associate at Center for Future Readiness at IMD Business School in Switzerland and Singapore.